What is FICO?

90% Of Top Lenders Use FICO Scores

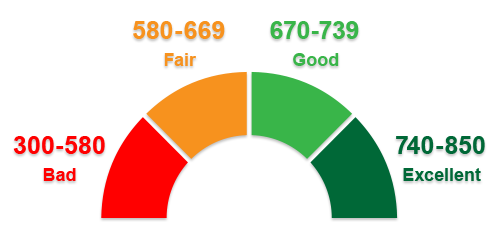

The first FICO scoring model was developed in 1989 by The Fair Isaac Corporation and has been an industry standard ever since. According to The Fair Isaac Corporation, 90% of top lenders use FICO scores to make lending judgements. VantageScore is another credit scoring model which was developed later in 2006 by the three major credit bureaus, Equifax, Experian, and TransUnion. Both FICO and VantageScore models use consumer credit reports to calculate a credit score between 300 and 850.

Your credit score is a value meant to provide lenders with an accurate prediction of whether or not an individual will fall at least 90 days behind on any payment within the next 2 years. VantageScore uses a model that can be used with any of the bureau reports, while FICO provides a unique score for each individual bureau. While the same information is used, scores can differ as much as 100 points between VantageScore and FICO models. Additionally, did you know that you even have multiple FICO scores? Depending on the type of loan you are applying for, the scoring model being used will change. For example, if you apply for an auto loan, the FICO Auto Score 8 model may be used. If you apply for credit card, the FICO Bankcard Score 5 model could be used to calculate your score.

Free credit score sites are quite popular these days and it is important to note that the model used will vary across these sites as well. When you view your credit score on CreditKarma.com, you are looking at scores based on the VantageScore model. Other sites may use the FICO score model to provide you with your score.

As you can see, our credit scores are actually quite complex. It is important not to get too hung up on these numbers. Focus on timely payments, reducing debt, and limiting your applications for unnecessary credit to improve your credit history over time.